Volatility Segmentation of SET100 Indices Using GARCH Models

Article Sidebar

Main Article Content

Abstract

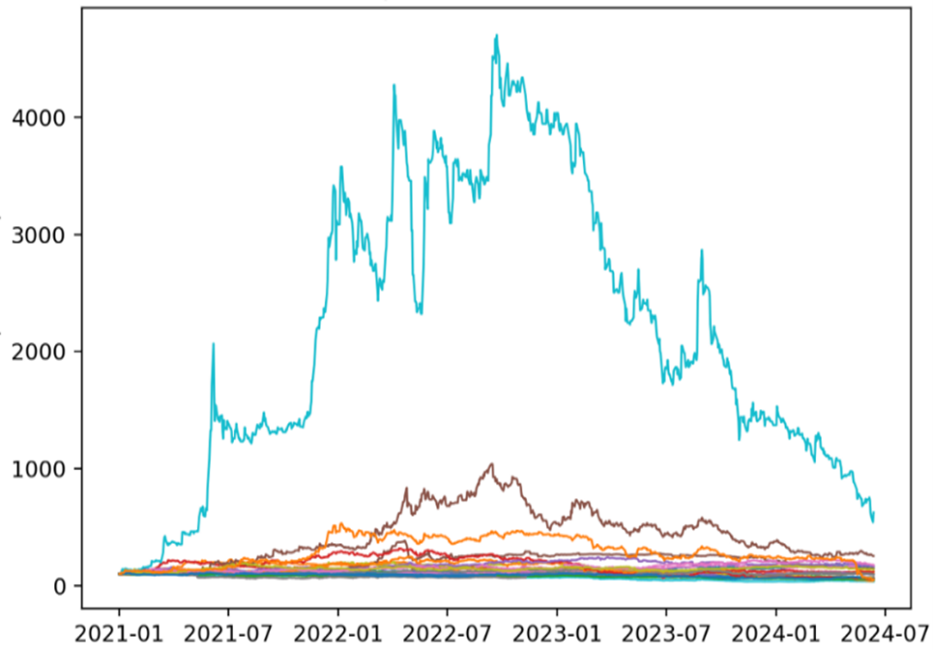

This study aims to examine the relationship between volatility and stock returns in the SET100 Index using daily closing price data. The GARCH (p, q) model is employed to forecast volatility, while the ARIMA model is used to forecast stock returns. The forecasted results are then used to classify stocks into four groups based on the median values of both forecasts. The empirical results indicate that volatility persistence, measured by the sum of the GARCH parameters (), is high and close to unity, reflecting the persistence of volatility in the Thai stock market. Over the 14-day forecasting horizon following the data endpoint, most stocks are classified into the high volatility–low return and low volatility–high return groups. Stocks identified as having investment potential due to high returns and low risk include TTB, TOP, WHA, RATCH, CENTEL, BCP, BCH, and BAM. The findings suggest that the proposed approach can be applied to support investment strategy planning.

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31(3): 307 - 327.

Buthprom, S. (2564). An Analysis of Stock Returns of Listed Companies in the SET100 Index in the Stock Exchange of Thailand. Master of Business Administration, Sukhothai Thammathirat Open University, Nonthaburi. 66 pages.

Challa, M.L., Malepati, V. and Kolusu, S.N. (2020). S&P BSE Sensex and S&P BSE IT return forecasting using ARIMA. Financial Innovation 6(1): Article 47. doi: 10.1186/s40854-020-00201-5.

Emenike, K.O. (2010). Modelling Stock Returns Volatility in Nigeria Using GARCH Models. In: Proceeding of International Conference on Management and Enterprise Development. University of Port Harcourt, Rivers State. 5 - 11.

Engle, R.F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50(4): 987 - 1007. doi: 10.2307/1912773.

Jiranyakul, K. (2545). Portfolio management strategy. Thai Journal of Development Administration. 42 (Special Issue: NIDA 36th Anniversary): 131 - 168.

Sharma, S., Aggarwal, V. and Yadav, M.P. (2021). Comparison of linear and non-linear GARCH models for forecasting volatility of select emerging countries. Journal of Advances in Management Research 18(4): 526 - 547. doi: 10.1108/JAMR-07-2020-0152.