Development of average run length formulas for EWMA control chart under the AR(1) with quadratic trend model for detecting and monitoring process variability

Keywords:

Average run length, AR(1) with quadratic trend, Explicit formulas, Numerical integral equationAbstract

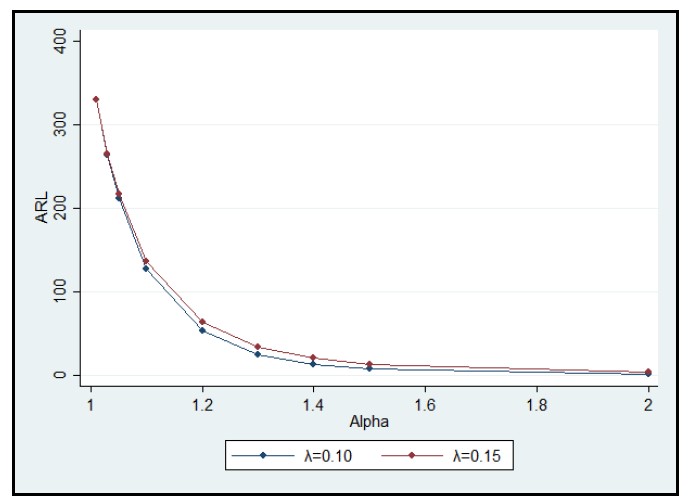

This paper proposes an explicit formula for calculating the average run length of an exponentially weighted moving average (EWMA) control chart based on the first-order autoregressive model with quadratic trends. Furthermore, the study presents a technique for estimating the average run length using the numerical integral equation (NIE) method. This enables a comparison between the results of the explicit formula and the numerical integral equation method. The two ARL solutions obtained from the explicit formula and numerical integral equation method are similar and identical with an absolute percentage difference of less than 0.001. Thereby, the explicit formula accurately corresponds to the NIE method. Additionally, the explicit formulas are more computationally efficient as they require fewer computations compared to the NIE approach

References

Areepong,Y., &Novikov,A. A. An integral equation approach for analysis of control charts[Doctoral’ thesis].University of Technology. 2009.

Busaba,J., Sukparungsee,S., Areepong,Y.,&Mititelu,G. (2012). Numerical approximations of average run length for AR(1) on exponential CUSUM. InProceedings of the International Muti Conference of Engineers and Computer Scientists, Hong Kong2012,7-10 March.

Champ, C. W., & Rigdon, S. E. (1991). A a comparison of the markov chain and the integral equation approaches for evaluating the run length distribution of quality control charts. Communications in Statistics-Simulation and Computation, 20(1), 191-204.

Crowder, S. V. (1987). A simple method for studying run–length distributions of exponentially weighted moving average charts. Technometrics, 29(4), 401-407.

Karoon, K., & Areepong, Y. (2023). Improving Sensitivity of the DEWMA Chart with Exact ARL Solution under the Trend AR (p) Model and Its Applications. Emerging Science Journal, 7(6), 1875-1891.

Karoon, K., Areepong, Y., & Sukparungsee, S. (2023). Modification of ARL for detecting changes on the double EWMA chart in time series data with the autoregressive model. Connection Science, 35(1), 2219040.

Karoon, K., Areepong, Y., & Sukparungsee, S. (2024). On the performance of the extended EWMA control chart for monitoring process mean based on autocorrelated data. Applied Science and Engineering Progress, 17(2), 6599-6599.

Lucas, J. M., & Saccucci, M. S. (1990). Exponentially weighted moving average control schemes: properties and enhancements. Technometrics, 32(1), 1-12.

Mititelu, G., Areepong, Y., Sukparungsee, S., & Novikov, A. (2010). Explicit analytical solutions for the average run length of CUSUM and EWMA charts. East-West Journal of Mathematics,1, 253-265.

Page, E. S. (1954). Continuous inspection schemes. Biometrika, 41(1/2), 100-115.

Peerajit, W. (2023). Statistical design of a one-sided CUSUM control chart to detect a mean shift in a FIMAX model with underlying exponential white noise. Thailand Statistician, 21(2), 397-420.

Petcharat, K., Areepong, Y., & Sukparungsee, S. (2013). Explicit formulas of average run length of EWMA chart for MA (q). Far East Journal of Mathematic Science, 78, 291 –300.

Petcharat, K. (2022). The effectivenessof CUSUM control chart for trend stationary seasonal autocorrelated data. Thailand Statistician, 20(2), 475-488.

Phanyaem, S. (2022). Explicit formulas and numerical integral equation of ARL for SARX (P, r) L model based on CUSUM chart. Mathematics and Statistics, 10(1), 88-99.

Phanthuna, P., Areepong, Y., & Sukparungsee, S. (2024). Performance Measurement of a DMEWMA Control Chart on an AR (p) Model with Exponential White Noise. Applied Science and Engineering Progress, 17(3), 7088-7088.

Roberts, S. W.(1959). Control chart tests based on geometric moving average. Technometrics, 1, 239-250.

Shewhart,W. A. (1931). Economic control of quality of manufactured product. Van Nostrand, New York.

Supharakonsakun, Y., & Areepong, Y. (2023). ARL Evaluation of a DEWMA Control Chart for Autocorrelated Data: A Case Study on Prices of Major Industrial Commodities. Emerging Science Journal, 7(5), 1771-1786.

Sunthornwat, R., Areepong, Y., & Sukparungsee, S. (2024). Evaluating the Performance of Modified EWMA Control Schemes for Serially Correlated Observations. Thailand Statistician, 22(3), 657-673.

Vanbrackle, L. N.,&Reynolds,M. R.(1997).EWMA and CUSUM control charts in the presence of correlation. Communications in Statistics-Simulation and Computation, 26(3),979-1008.

Downloads

Published

License

Copyright (c) 2024 Journal of Applied Science and Emerging Technology

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.