Improved GMM Estimator of AR(1) Process Near Unit Root

คำสำคัญ:

AR(1); GMM; mean square error; recursive mean adjustment.บทคัดย่อ

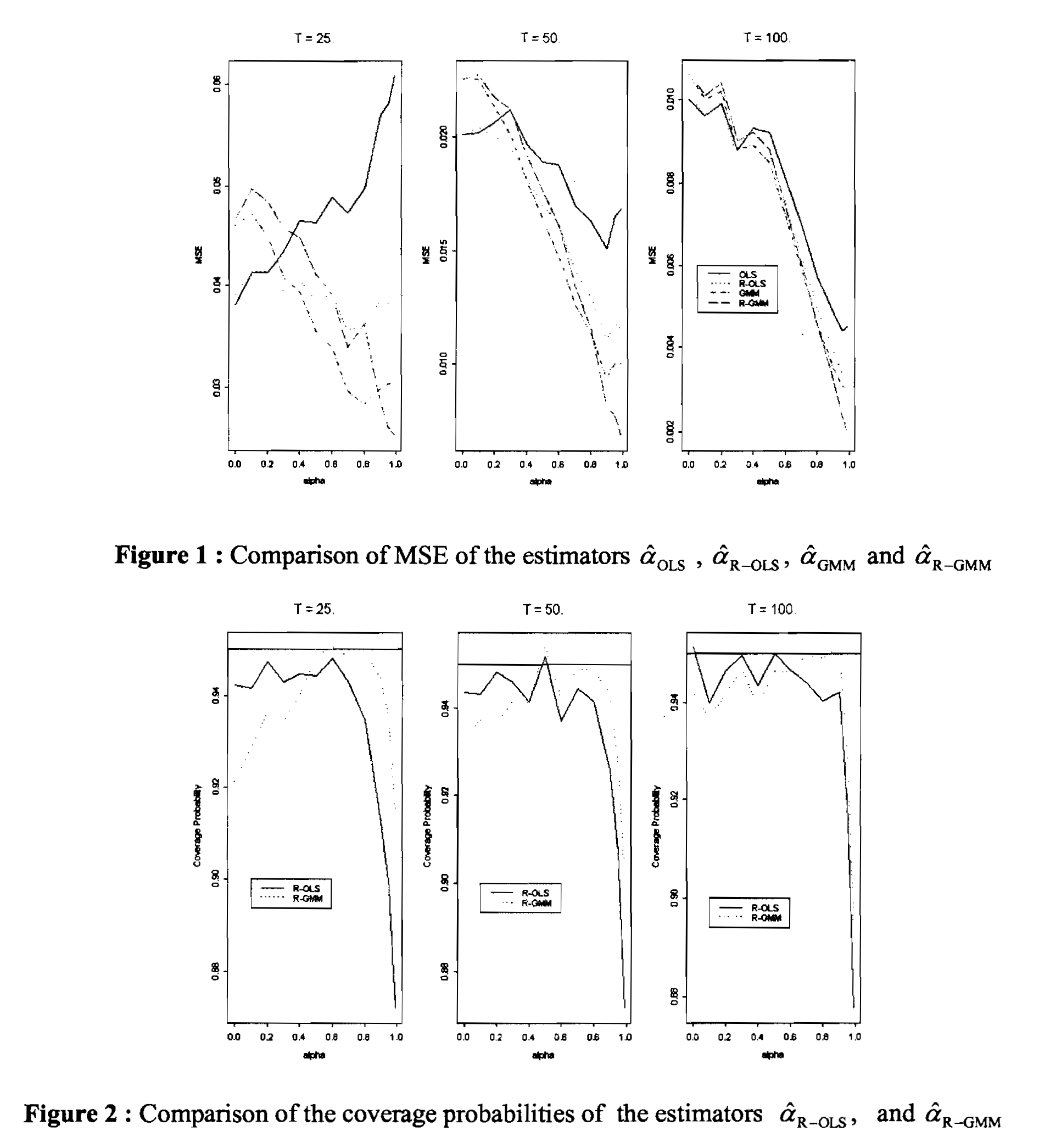

This paper presents the improved generalized method of moment (GMM) of Vougas (2000) by using the recursive mean adjustment of So and Shin (1999) in the context of a first-order autoregressive (AR(1)) process with non-zero mean. The limiting distribution of the new estimator is also included. The Monte Carlo simulations show that the new estimator produces smaller mean square error (MSE) than the recursive mean adjustment estimator of So and Shin (1999) when the autoregressive parameter approachs one for small sample sizes. Also the empirical coverage probabilities of the confidence intervals of the new autoregressive coefficient become close to the nominal level when the autoregressive parameter approachs one for small sample sizes.

Downloads

เผยแพร่แล้ว

2004-06-01

ฉบับ

บท

Research Articles